The Financial Supervision Commission has sent notification about its consent for the portfolio transfer from “UnipolSai Assicurazioni S.p.A.” to “Unipol Gruppo S.p.A.”

The Financial Supervision Commission (FSC) has been notified by the competent authority of Italy (INSTITUTO PER LA VIGILANZA SULLE ASSICURAZIONI (IVASS)) of the merger from the insurance undertaking “UnipolSai Assicurazioni S.p.A.” to “Unipol Gruppo S.p.A.”, including insurance contracts on which Bulgaria is a Member State where the risk is located. After reviewing the portfolio documents, the FSC decided to send a letter to the national competent authority of Italy on granting consent of the merger of “UnipolSai Assicurazioni S.p.A.” to “Unipol Gruppo S.p.A.”

After the merger “Unipol Gruppo S.p.A.” will change its name to “Unipol Assicurazioni S.p.A.” and will continue to operate on the territory of the Republic of Bulgaria under the conditions of the freedom to provide services.

There are prepared private pensions amendments whose primary objective is increasing old-age income and guaranteeing adequate pension benefits

In 2024 the Insurance and Private Pensions Committee of the Organization for Economic Co-operation and Development (OECD) carried out a research mission in Sofia which reviewed the supplementary pension insurance and assessed the compliance of the Bulgarian legislation and the supervisory activity with the OECD recommendations on the key principles for private pensions regulation.

As a result of the good partnership between the co-chairs – the Ministry of Finance and the Financial Supervision Commission (FSC), as well as the efforts of the Ministry of Labour and Social Policy, the representatives of other institutions, social partners and the industry, the review of the private pensions has already been successfully completed.

The Chair of the Working party on Private Pensions at the Insurance and Private Pensions Committee of the Organization for Economic Co-operation and Development (OECD) acknowledges the strengths of the supplementary pension insurance, including:

the multi-pillar pension model;

the stable legal framework;

the competent risk-based supervision.

The ability of the country to implement the OECD legal instruments and the excellent cooperation with the Bulgarian authorities during the review have been highly valued.

In this regard the OECD also notes the possibility for considering certain aspects that could contribute to improving the pension system that are in line with the philosophy of the possibilities for legislative amendments such as:

introduction of consumer choice between different investment strategies according to their life-cycle and risk tolerance (the so-called “multifunds model” encompassing funds with different investment profile);

review of the rules determining the investment opportunities to achieve growing profitability.

For this purpose, the competent institutions in the country should state clearly and in sync their commitment to the development of legislative amendments, the philosophy of which is supported in the context of the recommendations given by the OECD.

Joining the Organization for Economic Co-operation and Development is a key priority for the Republic of Bulgaria, in view of which the Financial Supervision Commission confirms its readiness and commitment to participate in the development of the pension system in the country in order to guarantee trust, fairness, stability and transparency.

The Financial Supervision Commission and the Bulgarian Association of Supplementary Pension Security Companies have started a dialogue and are ready to propose changes to the regulatory framework in the field of supplementary pension insurance, the ultimate goal of which is to increase the profitability of the management of the funds on the individual accounts of the citizens, respectively achieving an adequate replacement income upon withdrawal from the labor market (retirement).

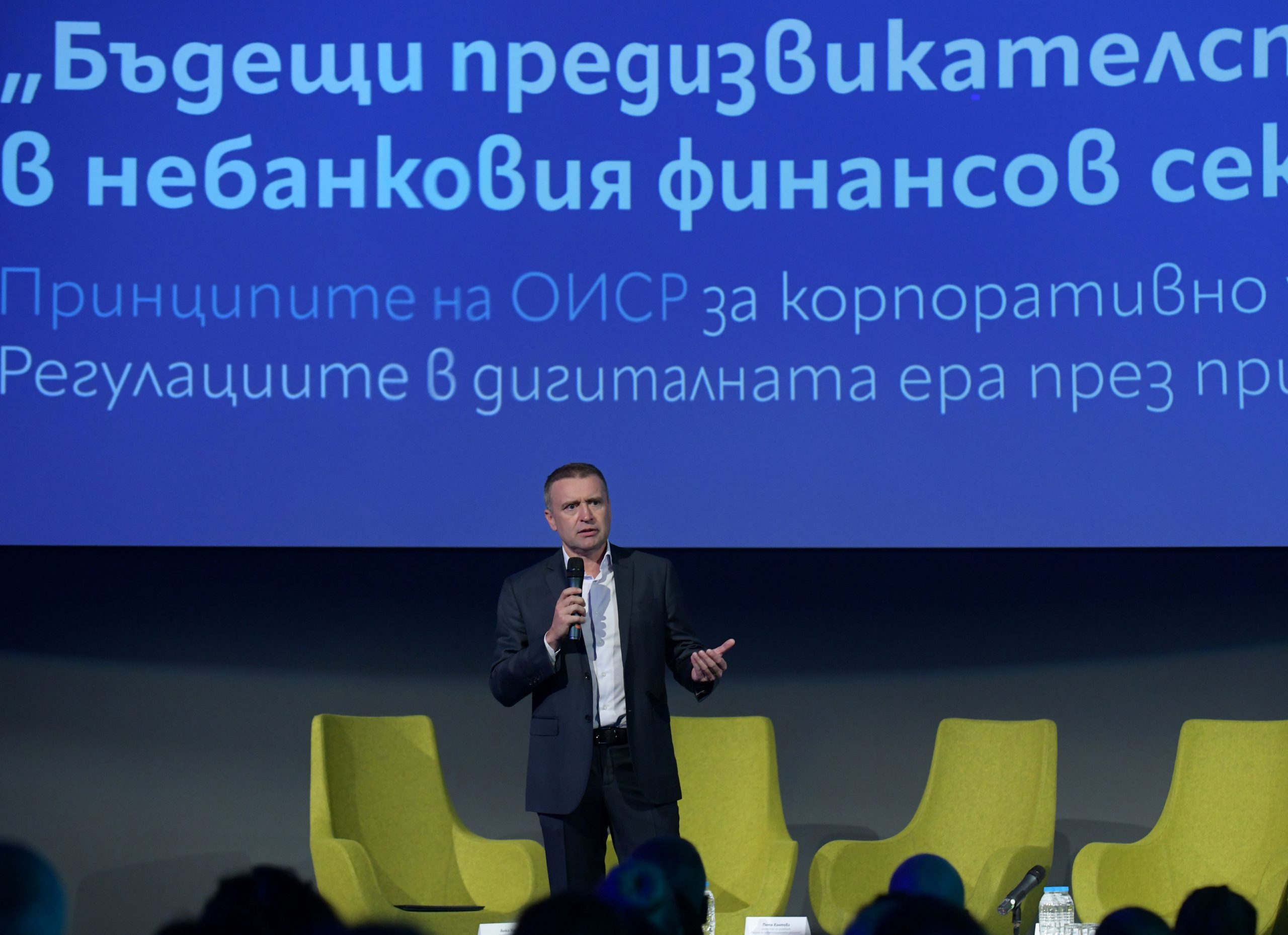

On July 10, the Financial Supervision Commission (FSC, the Commission) organized and held the extremely important for the non-banking financial sector conference “Future challenges and expectations in the non-banking financial sector”. At the Inter Expo Center in Sofia, over 300 participants, representatives of the investment, insurance and occupational pensions sectors took part in discussions, panels and presentations dedicated to the OECD principles of corporate governance in Bulgaria and the pan-European regulations – Regulation on the operational sustainability of digital technologies in the financial sector (DORA – Digital Operational Resilience Act) and the regulation on markets in crypto-assets (MiCA – Markets in Crypto-Assets).

Mr. Boyko Atanasov opened the conference with answers to the questions why the business and the regulator in the face of the FSC have a high-priority need for dialogue on the topic of new regulations in the non-banking financial sector. He shared with the participants that “The conference is a strategic initiative of the Financial Supervision Commission to promote a well-informed, collaborative and sustainable environment at the time of implementation of the two regulations, on which the future of digital finance will depend. It is our job to ensure that stakeholders are prepared to deal with the complexities of modern non-banking financial sector regulations and corporate governance.”

Boyko Atanasov – Chair of The Financial Supervision Commission

The audience of the live conference exceeded 300 participants – professionals and experts from the FSC, supervised entities – investment funds and intermediaries, insurance companies, occupational pensions companies, institutional partners, representatives of the business, the state, investors, consultants and the media. The FSC Chair and the moderator of the event encouraged an in-depth dialogue to identify solutions for specific cases, to share good practices and to develop strategies to effectively deal with the innovations faced by the non-banking financial sector in the country.

Boyko Atanasov also commented: “I believe that by proactively working and by sharing basic guidelines, we will facilitate the implementation of the principles and regulations regarding crypto–asset markets, we will help create a transparent and reliable financial system that benefits all interested parties. We will likely have challenges that we will overcome together and seek solutions to protect consumers. In a global and highly interconnected world, we must trust each other. Trust to overcome barriers and create a shared understanding of good corporate governance, promoting social responsibility and building a stable, sustainable and competitive economy.”

Boyko Atanasov – Chair of The Financial Supervision Commission

The conference was held in two main parts, with the first highlighting the OECD principles of corporate governance and regulatory compliance with a focus on sustainability, responsible investing and key ESG indicators for ethical impact assessment, and the second highlighting the challenges and core requirements of DORA and MiCA.

In addition to the FSC experts, who presented the OECD principles of corporate governance and the regulatory requirements of the two regulations, the event’s guest speakers and panelists were: Biserka Radeva – Director of the Network and Information Security Directorate at the Ministry of Electronic Government, Assoc. Prof., PhD, Mr. Manyu Moravenov – Member of the Board of Directors and Executive Director of the Bulgarian Stock Exchange, Kosta Yordanov – Executive Director and Deputy Chair of the Board of Directors of “Bianor Holding” AD, Stanislav Tanushev – Director of Investor Relations and Sustainability of “Sirma Group Holding” AD, Petko Petkov – Senior Manager of Consulting at Deloitte Bulgaria and Adelina Mitkova – Senior Manager at law firm Deloitte Legal.

The conference affected two regulations on which the future of digital finance will depend. Experts commented on the opportunities and challenges of DORA and MiCA, focusing on addressing growing cyber security threats and ensuring the stability of the financial system.

The principles of corporate governance will be a benchmark for Bulgarian companies that strive to align themselves with the best global practices, thus promoting a sustainable financial environment. This thesis was also the basis of the discussions on the introduction of the Code of Corporate Governance, which will set the standard for ethics, transparency and accountability, with the panelists also emphasizing the importance of corporate governance frameworks, their role in increasing investor confidence and ensuring sustainable growth.

Assoc. Prof. PhD. Manyu Moravenov pointed out that “corporate governance is the basis of the new business morality and the way companies should communicate with the public”. He noted that the latest amendments to the OECD principles are related to ESG policies and standards, and the ESG rating itself, which the Bulgarian Stock Exchange offers as a service through its partner LSEG Analytics, which is formed on the basis of a methodology in which more than 700 ESGs indicators are used, and 186 of them are comparable. He called upon public companies to obtain their ESG rating, and detailed information on the process which can be found on the Exchange’s page.

Assoc. Prof. PhD. Manyu Moravenov recommended that listed companies use the OXYGEN platform for reporting non-financial information – environmental, social and corporate aspects of the companies’ activities.

Ms. Petya Hantova – Director of the “Investments Supervision” Directorate, FSC, drew attention to the role of the regulator in the application of corporate governance principles, the legal framework and their main characteristics. Ms. Hantova pointed out that corporate governance includes a set of relationships between the company’s management, the board of directors, shareholders and stakeholders, and that each company should read the principles and implement them in the best way. Ms. Hantova also emphasized that the joint efforts of the regulator and capital market participants are the basis of ensuring its stability and transparency in building trust in investors, which in turn is a prerequisite for its development. She also noted that on a global scale, as well as in Bulgaria, the trend is becoming more and more prevalent, in which, when presenting a financial statement, investors are not so much interested in the figures inside, but in what is behind them – in the declaration of corporate governance to the non-financial information that is part of the reporting process.

The next panelist – Kosta Yordanov – Executive Director and Deputy Chair of the Board of Directors of “Bianor Holding” AD, drew attention to the fact that for the development of corporate governance in a company, steps must be taken to improve the work at the management level, as well as to increase investor confidence in the organization through open communication with them.

Stanislav Tanushev – Director of Investor Relations and Sustainability of “Sirma Group Holding” AD indicated that despite the numerous challenges in complying with the OECD Principles, they also provide many opportunities for direct positive results. He illustrates this with examples from “Sirma Group Holding” AD, where the care for nature and sustainability, and the installation of a photovoltaic plant of the company, also brings a direct financial result. Furthermore, how caring for employees leads to their job satisfaction and reduced turnover. Similar examples can be given for each of the Principles.

Panel 1: The OECD Principles of Corporate Governance in Bulgaria

Mrs. Yordanka Ushagelova – Director of “Analysis, Complaints and Restructuring” Directorate at the FSC drew attention to the challenges in introducing the Digital Operational Resilience Act. She pointed out that the purpose of the regulation is to introduce a comprehensive framework for digital operational resilience of EU financial entities. Ms. Ushagelova elaborated on the scope and significance of DORA.

Petko Petkov – Senior Manager “Consulting” at “Deloitte Bulgaria” explained that the Digital Operational Resilience Act “is not a revolution, but an evolution of already established norms”, which should introduce stricter requirements regarding cyber security . The panelist pointed out that there is an emerging drive for a coordinated approach in managing the risk arising from the use of digital technologies.

Biserka Radeva – Director of “Network and Information Security” Directorate in the Ministry of e-Government summarized the development over the years of the Law on Cyber Security and pointed out that at the moment there is a Law on Amendments and Supplements to the Law on Cyber Security based on the Directive (EU ) 2022/2555 of the European Parliament and of the Council of 14 December 2022 on measures for a high common level of cybersecurity across the Union, amending Regulation (EU) No 910/2014 and Directive (EU) 2018/1972, and repealing Directive (EU) 2016/1148 (NIS 2 Directive). Ms. Radeva pointed out the main pillars of NIS 2 – Member States’ responsibility, risk management and cooperation and information exchange. She also listed the similarities and differences between DORA and NIS2.

Adelina Mitkova – Senior Manager at Deloitte Legal law firm talks about the regulation on markets in crypto assets. She pointed out that this regulation is a “revolution rather than an evolution” and that it regulates the issuance, public offering and admission to trading of crypto-assets not covered by existing European legislation, as well as the conditions under which the services related to crypto-assets can be provided. Ms. Mitkova indicated which crypto-assets fall within the scope of the regulation, namely: asset-backed tokens, e-money tokens and all other consumer tokens. Mrs. Mitkova also noted what the main requirements are for the public offering of tokens. She concluded that MiCA will provide legal certainty to the crypto-asset market.

Mr. Milen Milev – Head of the “Regulation and Methodology” Department, Legal Directorate, FSC, spoke about the legal framework regarding the draft Law on Crypto Asset Markets and the measures that the Republic of Bulgaria will have to implement. He explicitly indicated that the Financial Supervision Commission was not unequivocally designated as the competent authority for the implementation of MiCA. He also indicated which persons fall within the scope of MiCA, namely the persons under Art. 4, items 38 and 39 of the Law on Measures Against Money Laundering.

The panelists agreed that the new regulations and their enforcement will increase investor confidence and contribute to increased security in the fight against money laundering and terrorist financing.

Panel 2: Regulation in the digital age through the lens of DORA and MiCA

The Financial Supervision Commission will continue to take a proactive approach to the implementation and oversight of European regulations, which are critical to addressing the complexities of digital transformation and maintaining capital market integrity. The non-banking financial sector and its development will rely on adherence to the principles of corporate governance and regulatory compliance – paramount to driving innovation, maintaining stability, effective governance and implementing regulatory best practices.

Below you can download the presentations presented during the Conference.

On the 5th of July 2024, in the premises of the Financial Supervision Commission a joint training addressed to the pension insurance companies was conducted by the FSC and the Financial Intelligence Directorate, State Agency for “National Security”. The training which was attended by total 18 representatives of all pension insurance companies in Bulgaria was focused on topics related to the implementation of the AML/CFT measures stipulated in the Law on Measures Against Money Laundering (LMML), the Law on Measures Against Financing of Terrorism (LMFT) and the acts on their implementation, as follows:

„New requirements stipulated in the LMML, Rules on implementation of the LMML (RILMML) and LMFT“ and

„Business-wide ML/TF risk assessment“.

The conducted training aimed to deepen the understanding of the representatives of the pension insurance companies licensed under the terms and conditions of the Social Insurance Code, with the exception of their activity of managing funds for supplementary compulsory pension insurance), for the importance to comply with the requirements of the preventive legislation, their essential role

Pursuant to art. 10, par. 5 of the Financial Supervision Commission Act, Mr. Petar Dzhelepov, Member of the Financial Supervision Commission (FSC), supporting the policy of analysis and assessment of risks in the financial markets, improvement of supervisory practice and protection of the interests of investors, insured and socially insured persons, has been designated as a deputy to carry out the functions of a Deputy Chairperson of FSC, leading “Investment Activity Supervision” Division.

Which, in your view, are the global trends in 2024 we could expect in the Fintech industry?

Boyko Atanasov: The Fintech industry is in a dynamic evolution state, whereat it incessantly reveals spectrum of innovations in front of us putting into question the established regulations. It is this industry, which namely provokes us to analyze the necessity of introducing progressive solutions accessible to a wider audience. I am deeply convinced that in the transforming financial ecosystem in 2024, services focused on personalized, secure and sustainable financial relationships, reflecting unprecedented technological advancement and consumer-centric innovation, will resonate.

In response to global trends in sustainability and environmental protection, this year we shall witness the rise of green (ESG) fintech trends, which will align financial technology with environmental considerations. Fintech solutions will evolve, so that by emphasizing both the sustainable investments and green financial activities, we will strive towards the goal of reducing the carbon footprint. The approach in question aims to connect technology with sustainability by strengthening the role of the financial sector in promoting practices that positively contribute to the environment and support global sustainability goals.

We are witnessing digitization in all of its aspects, including the use of blockchain and artificial intelligence (AI). In our role as regulator of the non-banking financial sector, it is very important for us to track innovative financing, evaluate new tools and practices, but at the same time protect consumers and act as a guarantor of the stability of the non-banking sector.

The advanced integration of artificial intelligence (AI) and machine learning (ML) will have significant impact on the customer experience, on the more precise detection and mitigation of fraudulent activities, and will optimize risk management strategies as well.

The development of these algorithms will lead to faster and more accurate financial solutions, invented to meet the unique needs and goals of individual users, so that we expect to enhance the level of their satisfaction and to increase their engagement.

The increased need for high cyber security will provide the basis for the protection of user data, tightly integrated in financial platforms. Improved features including advanced biometrics, multi-factor authentication and advanced encryption protocols will become ubiquitous elements of fintech security structure. These improvements will strengthen security barriers, protecting sensitive consumer information against potential threats and breaches, and maintaining integrity and trust in digital financial services.

How has the Financial Supervision Commission ensured adaptation of regulation to accommodate the evolving FinTech landscape in 2024?

Boyko Atanasov: It is important to note that regulatory approaches can vary in all jurisdictions. Specific adaptations will depend on regulations and priorities for each country or region, taking into account both technological progress and innovation as well as the European legislative framework.

FSC finalized the project for “Building a Unified Information System (UES). Since the autumn of 2023, the UES has been functioning successfully, and with its introduction, we report a significant improvement in the process of administrative service to citizens, businesses and supervised entities. All administrative services are fully accessible digitally. In addition to being part of the state administration system, in real time they are integrated with the activities and processes, and an exchange of information with the regulatory authorities of the EU – European Insurance and Occupational Pensions Authority (EIOPA) and the European Securities and Markets Authority (ESMA).

Of particular importance for 2024 will also be the regulations of crypto assets, as the dynamic nature of financial markets accentuates digital financial services, which are an increasingly important part of the European economic environment. Although the FSC has not been unequivocally designated as the national competent authority in this area, our daily work with the European regulators, in the face of ESMA, gives us the reason to be directly involved in this process and to follow the legislative changes, still at an initial level, but with the expectation that they will completely change the financial landscape of Europe. We are monitoring the implementation of the two acts: the European Digital Resilience Act (DORA) and the Markets in Crypto Assets Regulation (MiCA). The DORA Regulation, which entered into force in January 2023, aims to create a regulatory framework for digital operational resilience through which all companies can ensure that they can withstand all types of disruptions and threats related to information and communication technologies (ICT), with the aim of preventing and mitigating cyber threats. On the other hand, MiCA’s goal is to create a regulatory framework for the crypto asset market that supports innovation and harnesses the potential of crypto assets in a way that preserves financial stability and protects investors. EU countries must adopt national laws aligned with the regulation by June 2024, with full implementation starting in stages. DORA and MiCA will support innovation and the deployment of new financial technologies while ensuring an appropriate level of protection for consumers and investors.

Are there specific regulatory challenges or opportunities that the Bulgarian FinTech business may face in the current and the following years?

Boyko Atanasov: It is important for the Bulgarian FinTech business to keep up with the evolving regulatory environment, to engage in constant dialogue with the relevant industry associations and to seek legal advice in order to navigate the specific challenges and opportunities in the country. Some common challenges and opportunities for FinTech businesses in Bulgaria are the regulatory framework, licensing and authorization, data protection and privacy, risk management and cyber security.

As for the opportunities, they are: digital transformation, financial inclusion, cooperation with traditional institutions, government support and initiatives, and cross-border expansion.

How does the Financial Supervision Commission promote cooperation between traditional financial institutions and FinTech startups, especially in the non-banking sector?

Boyko Atanasov: The Financial Supervision Commission always proactively participates in cooperation programs and initiatives, provides regulatory guidance and support. Showing regulatory flexibility and sharing information is paying off. I believe that our continued partnership with the Bulgarian FinTech Association will contribute to promoting the creation of innovation centers and incubators.

The role of the FSC is to provoke the achievement of synchrony between the regulatory requirements and their implementation in a digital environment, with the ultimate goal being to reduce the administrative burden.

Part of the concrete results is the functioning Innovative Hub, providing a single point of contact with FinTech companies and the changed regulations for accessibility to the capital markets of small and medium-sized enterprises, the successfully functioning UES and the mobile application – FSC Mobile, the purpose of which is to help users and supervised entities, through the use of the most popular operating systems – Android and iOS.

The Financial Supervision Commission will continue to actively work and be in dialogue with the non-banking financial sector participants, as the result of the partnership between the national regulator and the business is the maintenance of a sustainable and innovation-friendly business environment.

The Financial Supervision Commission has sent notification about its consent for the portfolio transfer from Codan Forsikring A/S to Alm. Brand Forsikring A/S

The Financial Supervision Commission (FSC) has been notified by the competent authority of the Kingdom of Denmark (Danish Financial Supervisory Authority) of the forthcoming portfolio transfer from the insurance undertaking Codan Forsikring A/S to Alm. Brand Forsikring A/S, including insurance contracts on which the Republic of Bulgaria is a Member State where the risk is located. After reviewing the portfolio documents, the FSC decided to send a letter to the national competent authority of the Kingdom of Denmark on granting consent for the transfer of the insurance portfolio from Codan Forsikring A/S to Alm. Brand Forsikring A/S.

The Financial Supervision Commission has sent notification about its consent for the portfolio transfer from Aetna Health Insurance Company of Europe Designated Activity Company to AWL Health & Life

The Financial Supervision Commission was informed by the competent authority of the Republic of Ireland (Central Bank of Ireland) that the portfolio transfer from Aetna Health Insurance Company of Europe Designated Activity Company to AWL Health & Life was approved by the High Court of Ireland. The transfer was effected on 1 December 2023.